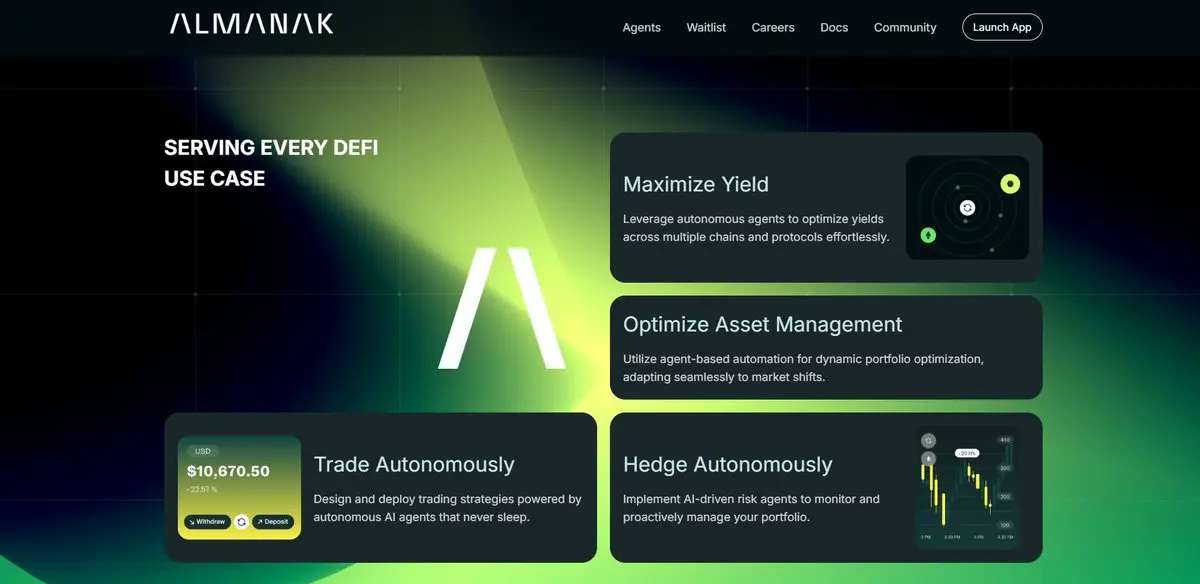

Imagine a crisis meeting at Goldman Sachs' Quant group: an intern replicated our Arbitrage model with

#Almanak# , zero code.

Select the volatility arbitrage template of Jump from the strategy library, input the parameters, and then deploy it. The entire process takes 8 minutes, and the assets never leave the cold wallet.

More critically, its Monte Carlo simulator backtested ten years of market data with on-chain data, achieving an error rate of <0.3%.

This seemingly cinematic scene is now being disrupted by the @Almanak__ project on the @cookiedotfun platform, utilizing no-code quantitative tra